Article is Written By

Fazlay Rabby James

Merchandiser

FCI BD Ltd.

Fazlay Rabby James

Merchandiser

FCI BD Ltd.

Costing: Costing is a very familiar word in Garments Industry and can be said as a heart of merchandising. It is also known as Cost sheet, Budget Sheet, BOM (Bill of Material) etc. Actually costing is nothing but a summation of different components price of a garments. But in garments industry especially for beginners costing is considered as very difficult task to learn. This article will give a brief idea about costing through which a beginner can easily understand how to calculate the garments price.

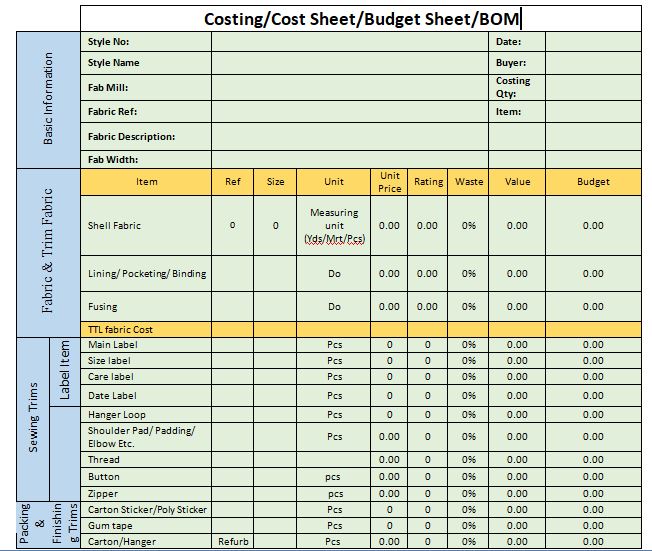

Below is a very common used table to do costing of a garments. Generally costing need to do in Microsoft Excel as to calculate the price of a garment some formulations are required. Before going through the costing procedure if we give an eye on below table then we will get a fair idea about costing format.

In above chart there is some sub category to understand a costing more easily. The aim of costing is to calculate FOB (Freight on Board/Free On Board) price of a garment as buyer buys a garment from a garment manufacturer by this FOB price.

Already I have stated that costing is just a summation of different components price of a garment. But assembling of different component price is not so easy. A merchandiser can’t put any item’s price (either Raw Material Price or consumption or SMV) in costing sheet from his assumption. Each and every item’s price has to be authentic. To get the single price, a merchant take support from different department of his factory to collect fabric consumption, SMV and also then different component price from different trims supplier.

In a nut shell we can tell that, Costing (FOB) = Fabric Cost + Trims Cost+ CM + Wash cost (If applicable)

To do a costing we must need below information.

1. Tech Pack/Design sketch/Sample of the particular garments with all necessary measurement.

2. FDS (Fabric Detail Sheet)

3. Mini Marker (Fabric Consumption)

4. Trims Price

5. SMV (Standard Minute Value)

6. Wash Cost (For Denim and Over dyed program)

2. FDS (Fabric Detail Sheet)

3. Mini Marker (Fabric Consumption)

4. Trims Price

5. SMV (Standard Minute Value)

6. Wash Cost (For Denim and Over dyed program)

Tech Pack/Design Sketch/Sample of the particular garments: It is the details deign sheet by which a pattern master can make a sample pattern and can make sample. This tech pack should have all necessary measurement. A tech pack should have mention all necessary operation, stitching details, component reference etc.

FDS (Fabric Details Sheet): FDS contains generally some basic and mandatory information of fabric like fabric price, composition etc. An FDS must need below information.

1. Fabric Unit Price

2. Fabric Cut able Width & Shrinkage Percentage (Without C/W mini marker cannot be made)

3. Fabric Article/reference number

4. Mill Name

5. Fabric Composition

Mini Marker: Mini Marker is a miniature version of marker which contain fabric consumption of a particular style of garments. CAD department do this part. To make mini marker we need

1. Tech Pack/Design sketch/Sample of the particular style with all necessary measurement.

2. Fabric Cut able Width & Shrinkage Percentage

1. Tech Pack/Design sketch/Sample of the particular style with all necessary measurement.

2. Fabric Cut able Width & Shrinkage Percentage

Trims Price: Trims Price is another important part of a costing. No garments can be made without trims and accordingly without trims price it is not possible to make a costing. A merchant can collect trims price directly from trims supplier. Sometimes buying merchant source the special trims as per buyer requirement and provide trims price to factory merchant for costing purpose.

SMV: It denotes Standard Minute Value that states the total number of minutes take to make a garment. Industrial Engineering departments are responsible to calculate SMV. It is calculated considering time of each operation. It is necessary to calculate CM of a garment.

Different Part of a Costing Sheet:

Basic Information: Each cost sheet contain some basic information by which anyone can get a rough idea about the product component and merchandiser can easily track the costing sheet for further use.

Different Part of a Costing Sheet:

Basic Information: Each cost sheet contain some basic information by which anyone can get a rough idea about the product component and merchandiser can easily track the costing sheet for further use.

Style No: Generally costing has been submitted to buyer after submit a new development sample. And each development sample has a individual style number by which we can track the style for any further use. E.g. 001, 002, Dev-A, Dev-B, 2018MAY01, 2018JUNE04 etc.

Style Name : Each styling isdesigned by a designer and a designer sometimes give a particular name of that style which name sometime give a basic concept about garment item. E.g. V neck Dress, Zip through Dress, Wide Leg Trouser, Ponte Leggings, Short Sleeve Blouse, Button Trough Blazer Etc.

Fabric Mill, Fabric Reference (Article No), Fabric Cut able Width:Fabric Mill name must need to mention in cost sheet. Otherwise it cannot be understand the fabric manufacturer of the garments.

Fabric Mill, Fabric Reference (Article No), Fabric Cut able Width:Fabric Mill name must need to mention in cost sheet. Otherwise it cannot be understand the fabric manufacturer of the garments.

Fabric Reference:Besides fabric mill name, fabric reference/fabric article number is necessary to track the fabric quality for further use. This fabric reference/article is a individual tracking number given by fabric manufacturer which is unique.

Fabric Description:Fabric description generally means the fabric composition, construction, GSM etc.

Fabric Cut able Width:It is the cut able width of a fabric which width is declared by fabric manufacturer. Fabric cut able width is very important to calculate the fabric consumption. Without fabric cut able width maker cannot be made and as a result consumption cannot be calculated.

Costing Quantity:In a costing generally we calculate FOB for per pcs garments. But besides calculate per PCS FOB we can also calculate total cost for each component for approximate order qty.

Wastage/Loading: Wastage/loading is wastage percentage considered for each individual item. It also vary from factory to factory based on their policy. Many factory considered wastage in fabric but many factory considered no wastage in fabric. But trims wastage must need for each factory and in that case generally sewing trims wastage is more than finishing trims wastage. Sometimes wastage percentage depends on order qty. If quantity less, then obviously wastage will be higher.

Fabric & Trims Fabric Cost: This is basically shell fabric and other trims fabric cost. Shell fabric means main body fabric and trims fabric means other supporting fabric, contrast fabric, pocketing, binding, piping etc. Fusing/interlining also consider in trims fabric category.

Trims Cost: This is all necessary trims cost for a garments.

Embellishment:Sometimes we have got special requirement from buyer such as printing, embroidery, heat seal etc. This is called embellishment. A garment manufacturer generally makes a garment but they may not have embroidery or print facility. In that case garments manufacturer do this part (embroidery/print) in other factory with an agreed unit price under permission from buyer. This is called sub contract production. And this total cost (including garments transportation cost to the third part factory) need to consider in embellishment cost sheet.

Wash: Sometimes buyer ask wash effect in garments. In that case if garments factory have not wash facility that case garments vendor do this part with other sub contract factory.

Test cost/ Courier Cost: This cost required based on buyer requirement and as per agreement with buyer. Every buyer have some testing requirement and this testing need to done in third party testing company like SGS, Intertek, UL, TUV etc. To make costing of a garments we need to consider some value for testing as testing charge.

Some buyer need some special sample like SMS (Sales Man Sample), Mock Shop Sample etc and buyer generally pay for this sampling cost and in that case we can considered this cost in costing sheet.

Commercial Cost /Transportation Cost:To ship a goods there is some cost involved which operation is done by commercial department. This is generally a fixed value or percentage value on total cost of a garments which value cover all shipment, transportation and commercial cost.

Some buyer need some special sample like SMS (Sales Man Sample), Mock Shop Sample etc and buyer generally pay for this sampling cost and in that case we can considered this cost in costing sheet.

Commercial Cost /Transportation Cost:To ship a goods there is some cost involved which operation is done by commercial department. This is generally a fixed value or percentage value on total cost of a garments which value cover all shipment, transportation and commercial cost.

Miscellaneous:No expenditure is possible without budget and this budget need to consider in particular style costing. To avoid any uncertain budget short generally every factory keep some value in hand as miscellaneous cost.

CM: In costing it denotes Cost of Making that refers the total manufacturing cost involved in making a garment. CM includes the factory operation cost to make the garments. CM of a garment depends on styling of a garment and also depends on factory standard. For easy style CM is less and in such a way for critical style CM is higher. In fact it is related with SMV and overhead cost of the respective production unit.

Therefor, to calculate accurate CM of a garment we have to consider SMV of a garment. Also each factory has e fixed CPM (Cost per Minitue) / EPM (Earn per Minitue). If we multiply this standard CPM with SMV then we will get CM of that garments. Basically CM offer is the main output of experience of a merchandiser. By the basic rules fixed by a factory management (SMVXCPM=CM) we can calculate CM but to offer more logical CM a merchandiser should have proper market knowledge about product price. By this knowledge a merchandiser can bring the business for his company by offering logical, sharp but profitable CM.

Therefor, to calculate accurate CM of a garment we have to consider SMV of a garment. Also each factory has e fixed CPM (Cost per Minitue) / EPM (Earn per Minitue). If we multiply this standard CPM with SMV then we will get CM of that garments. Basically CM offer is the main output of experience of a merchandiser. By the basic rules fixed by a factory management (SMVXCPM=CM) we can calculate CM but to offer more logical CM a merchandiser should have proper market knowledge about product price. By this knowledge a merchandiser can bring the business for his company by offering logical, sharp but profitable CM.

FOB without buying commission: If we sum the fabric cost, trims cost, commercial cost, miscellaneous cost and CM then we will get the garments FOB. But this FOB is without any buying commission. Generally we take order through local buying house and there have an agreement with factory and buying house that factory will pay a certain percentage of FOB as commission for confirmed order.

Garments FOB: If we add this buying commission with total cost then we will get actual garments FOB which price we can sell the product to buyer.

Offered FOB & Profit: Garments FOB is the total cost of a garment making including raw materials cost & CM. To keep some margin on each order factory need to offer final price with some additional invisible cost as there will be some negotiation to place an order finally.

Need to input all the individual prices in excel sheet to that is already formulated for costing and then check with your seniors or department head to offer this to buyer.

Garments Costing Procedure | Woven Garment Costing | Different Terms of Costing

Advertisements

Article is Written By

Fazlay Rabby James

Merchandiser

FCI BD Ltd.

Fazlay Rabby James

Merchandiser

FCI BD Ltd.

Costing: Costing is a very familiar word in Garments Industry and can be said as a heart of merchandising. It is also known as Cost sheet, Budget Sheet, BOM (Bill of Material) etc. Actually costing is nothing but a summation of different components price of a garments. But in garments industry especially for beginners costing is considered as very difficult task to learn. This article will give a brief idea about costing through which a beginner can easily understand how to calculate the garments price.

Below is a very common used table to do costing of a garments. Generally costing need to do in Microsoft Excel as to calculate the price of a garment some formulations are required. Before going through the costing procedure if we give an eye on below table then we will get a fair idea about costing format.

In above chart there is some sub category to understand a costing more easily. The aim of costing is to calculate FOB (Freight on Board/Free On Board) price of a garment as buyer buys a garment from a garment manufacturer by this FOB price.

Already I have stated that costing is just a summation of different components price of a garment. But assembling of different component price is not so easy. A merchandiser can’t put any item’s price (either Raw Material Price or consumption or SMV) in costing sheet from his assumption. Each and every item’s price has to be authentic. To get the single price, a merchant take support from different department of his factory to collect fabric consumption, SMV and also then different component price from different trims supplier.

In a nut shell we can tell that, Costing (FOB) = Fabric Cost + Trims Cost+ CM + Wash cost (If applicable)

To do a costing we must need below information.

1. Tech Pack/Design sketch/Sample of the particular garments with all necessary measurement.

2. FDS (Fabric Detail Sheet)

3. Mini Marker (Fabric Consumption)

4. Trims Price

5. SMV (Standard Minute Value)

6. Wash Cost (For Denim and Over dyed program)

2. FDS (Fabric Detail Sheet)

3. Mini Marker (Fabric Consumption)

4. Trims Price

5. SMV (Standard Minute Value)

6. Wash Cost (For Denim and Over dyed program)

Tech Pack/Design Sketch/Sample of the particular garments: It is the details deign sheet by which a pattern master can make a sample pattern and can make sample. This tech pack should have all necessary measurement. A tech pack should have mention all necessary operation, stitching details, component reference etc.

FDS (Fabric Details Sheet): FDS contains generally some basic and mandatory information of fabric like fabric price, composition etc. An FDS must need below information.

1. Fabric Unit Price

2. Fabric Cut able Width & Shrinkage Percentage (Without C/W mini marker cannot be made)

3. Fabric Article/reference number

4. Mill Name

5. Fabric Composition

Mini Marker: Mini Marker is a miniature version of marker which contain fabric consumption of a particular style of garments. CAD department do this part. To make mini marker we need

1. Tech Pack/Design sketch/Sample of the particular style with all necessary measurement.

2. Fabric Cut able Width & Shrinkage Percentage

1. Tech Pack/Design sketch/Sample of the particular style with all necessary measurement.

2. Fabric Cut able Width & Shrinkage Percentage

Trims Price: Trims Price is another important part of a costing. No garments can be made without trims and accordingly without trims price it is not possible to make a costing. A merchant can collect trims price directly from trims supplier. Sometimes buying merchant source the special trims as per buyer requirement and provide trims price to factory merchant for costing purpose.

SMV: It denotes Standard Minute Value that states the total number of minutes take to make a garment. Industrial Engineering departments are responsible to calculate SMV. It is calculated considering time of each operation. It is necessary to calculate CM of a garment.

Different Part of a Costing Sheet:

Basic Information: Each cost sheet contain some basic information by which anyone can get a rough idea about the product component and merchandiser can easily track the costing sheet for further use.

Different Part of a Costing Sheet:

Basic Information: Each cost sheet contain some basic information by which anyone can get a rough idea about the product component and merchandiser can easily track the costing sheet for further use.

Style No: Generally costing has been submitted to buyer after submit a new development sample. And each development sample has a individual style number by which we can track the style for any further use. E.g. 001, 002, Dev-A, Dev-B, 2018MAY01, 2018JUNE04 etc.

Style Name : Each styling isdesigned by a designer and a designer sometimes give a particular name of that style which name sometime give a basic concept about garment item. E.g. V neck Dress, Zip through Dress, Wide Leg Trouser, Ponte Leggings, Short Sleeve Blouse, Button Trough Blazer Etc.

Fabric Mill, Fabric Reference (Article No), Fabric Cut able Width:Fabric Mill name must need to mention in cost sheet. Otherwise it cannot be understand the fabric manufacturer of the garments.

Fabric Mill, Fabric Reference (Article No), Fabric Cut able Width:Fabric Mill name must need to mention in cost sheet. Otherwise it cannot be understand the fabric manufacturer of the garments.

Fabric Reference:Besides fabric mill name, fabric reference/fabric article number is necessary to track the fabric quality for further use. This fabric reference/article is a individual tracking number given by fabric manufacturer which is unique.

Fabric Description:Fabric description generally means the fabric composition, construction, GSM etc.

Fabric Cut able Width:It is the cut able width of a fabric which width is declared by fabric manufacturer. Fabric cut able width is very important to calculate the fabric consumption. Without fabric cut able width maker cannot be made and as a result consumption cannot be calculated.

Costing Quantity:In a costing generally we calculate FOB for per pcs garments. But besides calculate per PCS FOB we can also calculate total cost for each component for approximate order qty.

Wastage/Loading: Wastage/loading is wastage percentage considered for each individual item. It also vary from factory to factory based on their policy. Many factory considered wastage in fabric but many factory considered no wastage in fabric. But trims wastage must need for each factory and in that case generally sewing trims wastage is more than finishing trims wastage. Sometimes wastage percentage depends on order qty. If quantity less, then obviously wastage will be higher.

Fabric & Trims Fabric Cost: This is basically shell fabric and other trims fabric cost. Shell fabric means main body fabric and trims fabric means other supporting fabric, contrast fabric, pocketing, binding, piping etc. Fusing/interlining also consider in trims fabric category.

Trims Cost: This is all necessary trims cost for a garments.

Embellishment:Sometimes we have got special requirement from buyer such as printing, embroidery, heat seal etc. This is called embellishment. A garment manufacturer generally makes a garment but they may not have embroidery or print facility. In that case garments manufacturer do this part (embroidery/print) in other factory with an agreed unit price under permission from buyer. This is called sub contract production. And this total cost (including garments transportation cost to the third part factory) need to consider in embellishment cost sheet.

Wash: Sometimes buyer ask wash effect in garments. In that case if garments factory have not wash facility that case garments vendor do this part with other sub contract factory.

Test cost/ Courier Cost: This cost required based on buyer requirement and as per agreement with buyer. Every buyer have some testing requirement and this testing need to done in third party testing company like SGS, Intertek, UL, TUV etc. To make costing of a garments we need to consider some value for testing as testing charge.

Some buyer need some special sample like SMS (Sales Man Sample), Mock Shop Sample etc and buyer generally pay for this sampling cost and in that case we can considered this cost in costing sheet.

Commercial Cost /Transportation Cost:To ship a goods there is some cost involved which operation is done by commercial department. This is generally a fixed value or percentage value on total cost of a garments which value cover all shipment, transportation and commercial cost.

Some buyer need some special sample like SMS (Sales Man Sample), Mock Shop Sample etc and buyer generally pay for this sampling cost and in that case we can considered this cost in costing sheet.

Commercial Cost /Transportation Cost:To ship a goods there is some cost involved which operation is done by commercial department. This is generally a fixed value or percentage value on total cost of a garments which value cover all shipment, transportation and commercial cost.

Miscellaneous:No expenditure is possible without budget and this budget need to consider in particular style costing. To avoid any uncertain budget short generally every factory keep some value in hand as miscellaneous cost.

CM: In costing it denotes Cost of Making that refers the total manufacturing cost involved in making a garment. CM includes the factory operation cost to make the garments. CM of a garment depends on styling of a garment and also depends on factory standard. For easy style CM is less and in such a way for critical style CM is higher. In fact it is related with SMV and overhead cost of the respective production unit.

Therefor, to calculate accurate CM of a garment we have to consider SMV of a garment. Also each factory has e fixed CPM (Cost per Minitue) / EPM (Earn per Minitue). If we multiply this standard CPM with SMV then we will get CM of that garments. Basically CM offer is the main output of experience of a merchandiser. By the basic rules fixed by a factory management (SMVXCPM=CM) we can calculate CM but to offer more logical CM a merchandiser should have proper market knowledge about product price. By this knowledge a merchandiser can bring the business for his company by offering logical, sharp but profitable CM.

Therefor, to calculate accurate CM of a garment we have to consider SMV of a garment. Also each factory has e fixed CPM (Cost per Minitue) / EPM (Earn per Minitue). If we multiply this standard CPM with SMV then we will get CM of that garments. Basically CM offer is the main output of experience of a merchandiser. By the basic rules fixed by a factory management (SMVXCPM=CM) we can calculate CM but to offer more logical CM a merchandiser should have proper market knowledge about product price. By this knowledge a merchandiser can bring the business for his company by offering logical, sharp but profitable CM.

FOB without buying commission: If we sum the fabric cost, trims cost, commercial cost, miscellaneous cost and CM then we will get the garments FOB. But this FOB is without any buying commission. Generally we take order through local buying house and there have an agreement with factory and buying house that factory will pay a certain percentage of FOB as commission for confirmed order.

Garments FOB: If we add this buying commission with total cost then we will get actual garments FOB which price we can sell the product to buyer.

Offered FOB & Profit: Garments FOB is the total cost of a garment making including raw materials cost & CM. To keep some margin on each order factory need to offer final price with some additional invisible cost as there will be some negotiation to place an order finally.

Need to input all the individual prices in excel sheet to that is already formulated for costing and then check with your seniors or department head to offer this to buyer.

Advertisements