Article is Written By

Fazlay Rabby James

Merchandiser

FCI BD Ltd.

Fazlay Rabby James

Merchandiser

FCI BD Ltd.

We are here to share an example of making cost sheet where a linned jacket has been considered.

Below is an example of the Garment Specification sheet or Tech Pack (Technical Package):

Step 1: At first we have to collect FDS for shell fabric & trims fabric. Let us consider all shell fabric & trims fabric price in one sheet as bellow.

Step 2: Now we have to send mini marker request to CAD department of your factory for consumption of all shell fabric & trim fabric. Then we have to send design pack with all shell fabric & trim fabric cut able width. In return CAD departments will send us mini marker (consumption) for all fabric and trims fabric. Sometimes it may call YY (yield yardage).

Example of a mini marker

The style we are taking for experiment, here we will get total 9 mini marker from CAD department as bellow.

1. Shell Fabric

2. Body Lining

3. Sleeve Lining

4. Piping

5. Inside Pocket + Pocket Envelop (since both are same quality; 210T Taffeta Black, so two parts will be integrated in one marker)

6. Knit Fusing

7. Paper Fusing

8. Thread Fusing

Let us consider consumption is as bellow for per pcs garments.

1. Shell Fabric---------2.2 yds

2. Body Lining--------1.3 yds

3. Sleeve Lining-----0.90 yds

4. Piping-------------0.12 yds

5. Inside Pocket + Pocket Envelop----0.06yds

6. Knit Fusing-----0.65yds

7. Paper Fusing—1.10yds

8. Thread Fusing-0.17 yds

Step 3:

We have to send the tech pack to our IE department’s concern engineer to calculate SMV.

Let us consider garments SMV is coming 65 minutes.

Also let us consider factory standard CPM is nearer to 0.07 so our target CM will be about 4.55 (65X0.07=4.55). Here I have calculated CM putting a formula which is mainly depends of factory standard. Also sometimes it is not possible to consider accurate & market competitive CM as per factory standard. In that case merchant need to use his experience to offer perfect CM to grab the business also keeping company profit.

Step 4:

- Main Label—$0.05/pcs

- Size Label--$0.02/pcs

- Care Label-$0.03/pcs

- Hang Tag-$0.05/pcs

- Thread-$1.5/cone (Let us consider thread consumption is 0.2 cone/pcs garments.

- Poly-$0.10/pcs

- Carton-$1.50/ pcs (Let us consider 5 pcs garments can be packed in one pcs carton so carton consumption will be 1/5)

- Gum tape-$0.50/pcs (Let us consider 15 pcs carton can be packed by one pcs gumtape so gum tape consumption for per pcs garments will be 1/(5X15))

- Button-0.05/pcs

- Carton Sticker-$0.10/ pcs (Let us consider 5 pcs garments can be packed in one pcs carton so carton sticker consumption will be 1/5)

Step 5:

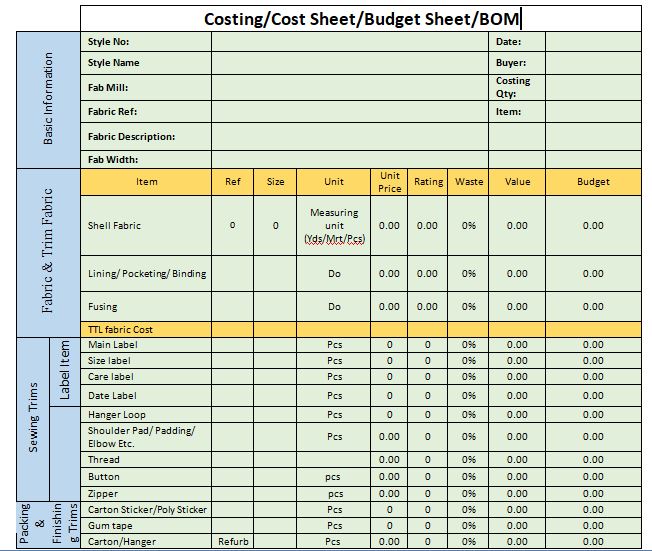

Already we have got all shell fabric & trims fabric price in FDS, now we can make cost sheet following above prices.

Though here profit is showing $0.82 if it is accepted by buyer but net profit will be higher than this. All factories have minimum profit limit to grab orders so this philosophy is different for respective factories.

Retail Price: The selling price of product in shop is the retail price of the product. Buyer purchase the garments from factory in FOB price. But they also sell the garments in shop considering all cost involved in taking orders to store including company management cost with margin or profit. Depending upon customer and quality of product the retail prices become three to ten times than FOB price.

Garments Costing With Example | Practical Method of Garments Costing | Overview of Woven Jacket Costing

Advertisements

Article is Written By

Fazlay Rabby James

Merchandiser

FCI BD Ltd.

Fazlay Rabby James

Merchandiser

FCI BD Ltd.

We are here to share an example of making cost sheet where a linned jacket has been considered.

Below is an example of the Garment Specification sheet or Tech Pack (Technical Package):

Step 1: At first we have to collect FDS for shell fabric & trims fabric. Let us consider all shell fabric & trims fabric price in one sheet as bellow.

Step 2: Now we have to send mini marker request to CAD department of your factory for consumption of all shell fabric & trim fabric. Then we have to send design pack with all shell fabric & trim fabric cut able width. In return CAD departments will send us mini marker (consumption) for all fabric and trims fabric. Sometimes it may call YY (yield yardage).

Example of a mini marker

The style we are taking for experiment, here we will get total 9 mini marker from CAD department as bellow.

1. Shell Fabric

2. Body Lining

3. Sleeve Lining

4. Piping

5. Inside Pocket + Pocket Envelop (since both are same quality; 210T Taffeta Black, so two parts will be integrated in one marker)

6. Knit Fusing

7. Paper Fusing

8. Thread Fusing

Let us consider consumption is as bellow for per pcs garments.

1. Shell Fabric---------2.2 yds

2. Body Lining--------1.3 yds

3. Sleeve Lining-----0.90 yds

4. Piping-------------0.12 yds

5. Inside Pocket + Pocket Envelop----0.06yds

6. Knit Fusing-----0.65yds

7. Paper Fusing—1.10yds

8. Thread Fusing-0.17 yds

Step 3:

We have to send the tech pack to our IE department’s concern engineer to calculate SMV.

Let us consider garments SMV is coming 65 minutes.

Also let us consider factory standard CPM is nearer to 0.07 so our target CM will be about 4.55 (65X0.07=4.55). Here I have calculated CM putting a formula which is mainly depends of factory standard. Also sometimes it is not possible to consider accurate & market competitive CM as per factory standard. In that case merchant need to use his experience to offer perfect CM to grab the business also keeping company profit.

Step 4:

- Main Label—$0.05/pcs

- Size Label--$0.02/pcs

- Care Label-$0.03/pcs

- Hang Tag-$0.05/pcs

- Thread-$1.5/cone (Let us consider thread consumption is 0.2 cone/pcs garments.

- Poly-$0.10/pcs

- Carton-$1.50/ pcs (Let us consider 5 pcs garments can be packed in one pcs carton so carton consumption will be 1/5)

- Gum tape-$0.50/pcs (Let us consider 15 pcs carton can be packed by one pcs gumtape so gum tape consumption for per pcs garments will be 1/(5X15))

- Button-0.05/pcs

- Carton Sticker-$0.10/ pcs (Let us consider 5 pcs garments can be packed in one pcs carton so carton sticker consumption will be 1/5)

Step 5:

Already we have got all shell fabric & trims fabric price in FDS, now we can make cost sheet following above prices.

Though here profit is showing $0.82 if it is accepted by buyer but net profit will be higher than this. All factories have minimum profit limit to grab orders so this philosophy is different for respective factories.

Retail Price: The selling price of product in shop is the retail price of the product. Buyer purchase the garments from factory in FOB price. But they also sell the garments in shop considering all cost involved in taking orders to store including company management cost with margin or profit. Depending upon customer and quality of product the retail prices become three to ten times than FOB price.

Advertisements